new clients - Students/seniors $35 - Corp tax filing starts $800 - install app

Choosing between a sole proprietorship and a corporation in Canada? Learn the key differences in taxes, liability, and compliance for small businesses.

Choosing between a sole proprietorship and a corporation in Canada? Learn the key differences in taxes, liability, and compliance for small businesses.

12/20/20252 min read

Understanding Your Business Structure Options

One of the first and most important decisions Canadian small business owners make is choosing a business structure. The two most common options are sole proprietorship and corporation—each with its own tax implications, legal responsibilities, and costs.

Understanding these differences can help you avoid unnecessary taxes and compliance issues.

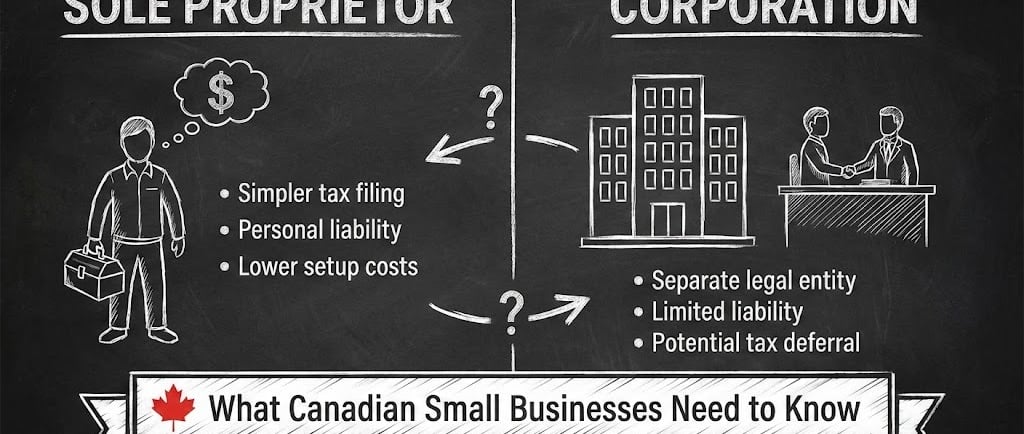

What Is a Sole Proprietorship?

A sole proprietorship is the simplest business structure. You and your business are considered the same legal entity.

Key Features:

Easy and inexpensive to set up

Business income reported on your personal tax return

Full personal responsibility for business debts and liabilities

This structure is common for freelancers, consultants, and new business owners.

What Is a Corporation?

A corporation is a separate legal entity from its owner(s). It earns income, pays corporate taxes, and exists independently.

Key Features:

Separate corporate tax return (T2)

Lower corporate tax rates on active business income

Limited liability protection

More compliance and administrative requirements

Key Differences: Sole Proprietor vs. Corporation

1. Taxation

Sole Proprietor: Business income is taxed at personal marginal tax rates.

Corporation: Income is taxed at corporate rates, with potential tax deferral if profits are retained.

2. Liability

Sole Proprietor: Personally liable for all business debts and legal claims.

Corporation: Generally offers limited liability protection.

3. Costs & Complexity

Sole Proprietor: Minimal setup and ongoing costs.

Corporation: Higher costs due to accounting, legal, and filing requirements.

4. Access to Tax Planning

Corporations provide more opportunities for:

Income deferral

Salary vs. dividend planning

Long-term business growth strategies

Which Option Is Right for Your Business?

A sole proprietorship may be right if you:

Are just starting out

Earn modest or inconsistent income

Want simplicity and low costs

A corporation may be better if you:

Earn consistent profits

Want to defer personal taxes

Face higher business risk

Plan to grow or sell your business

Common Misconceptions

Incorporation does not automatically reduce taxes if all income is withdrawn personally.

Corporations still require proper bookkeeping and compliance.

Switching structures later is possible but should be planned carefully.

How TiKi Tax Helps Small Businesses

At TiKi Tax, we help Canadian small businesses choose the right structure based on tax efficiency, risk, and long-term goals.

We offer:

Business structure analysis

Tax comparisons and projections

Incorporation services

Ongoing tax and bookkeeping support

Our approach is practical, transparent, and tailored to your situation.

Make the Right Choice from the Start

Choosing the wrong structure can cost you time and money. Getting the right advice early helps your business grow with confidence.

👉 Visit https://www.tikitax.ca/ to speak with a tax professional and get personalized guidance for your small business.

Services

Personalized tax preparation and consulting for all.

Location:

Support

email: info@tikitax.com

Phone:(+1).236.788.7799

© 2024. All rights reserved.

2339 HW 97, Kelowna, BC, Canada

145 Chadwick Ct Suite 220, North Vancouver, BC V7M 3K1